HOW TO SET UP YOUR BOOKS FOR CONSTRUCTION ACCOUNTING … AND WHAT IS

EARNED REVENUE?

In most ordinary businesses, accounting is heavily focused on:

Receivables

Cash Received

Sales Invoices

And Expenses

BUT construction accounting works differently because jobs can last for many months--or even years--and the money coming in does not always match the actual progress of the work.

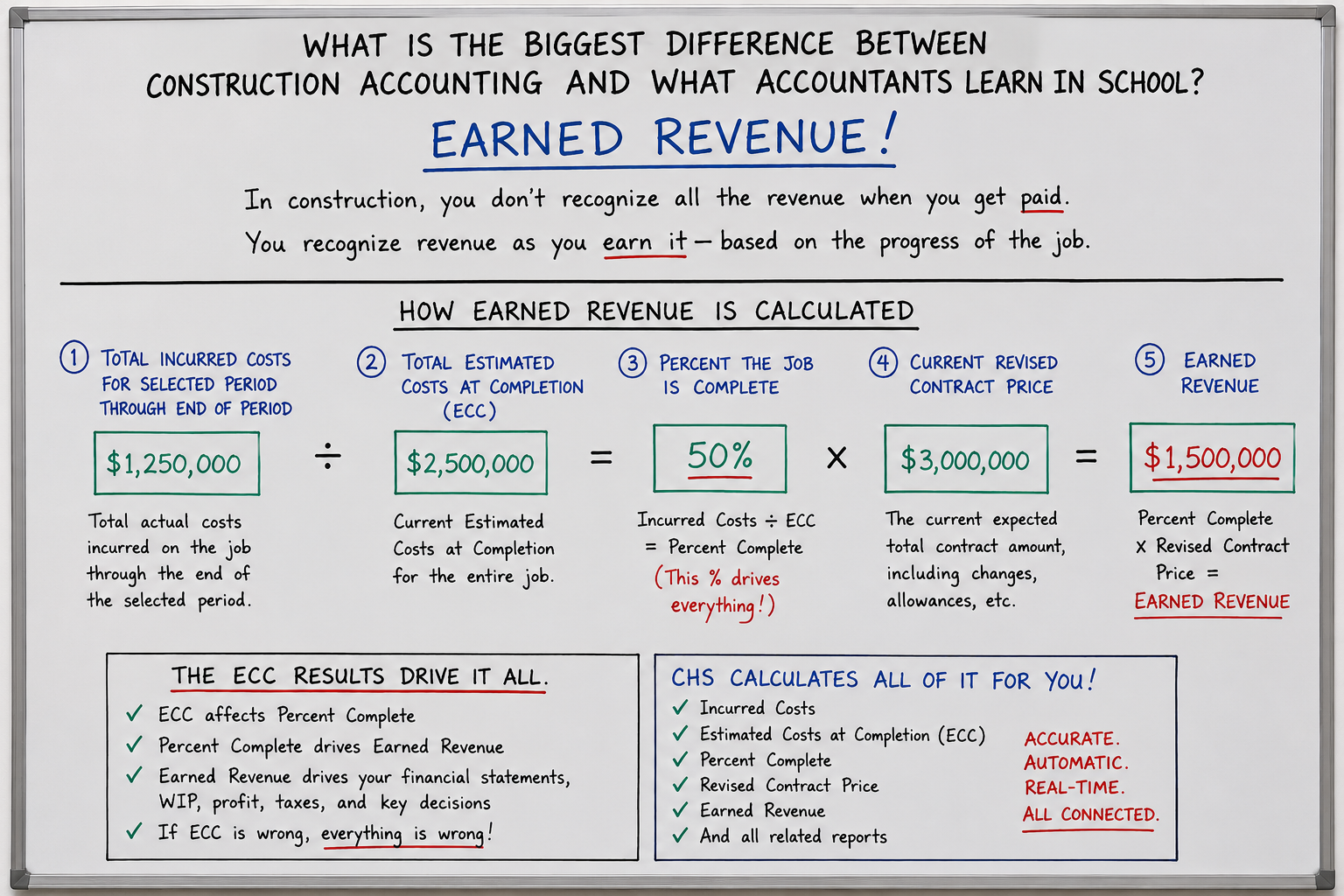

Per GAAP and the IRS: In construction, you shouldn’t *recognize revenue when you get paid. You *recognize revenue as you EARN it — based on the progress of the job.

*“Recognize” means when you post revenues to a Sales account that will be included on an Income Statement.

To “recognize revenue” means:

*To officially record revenue on the income statement because it has been earned.

In construction accounting, revenue is not recognized simply because:

You sent an invoice

Received a deposit

Or collected cash

Instead, revenue is recognized based on:

The progress of the job.

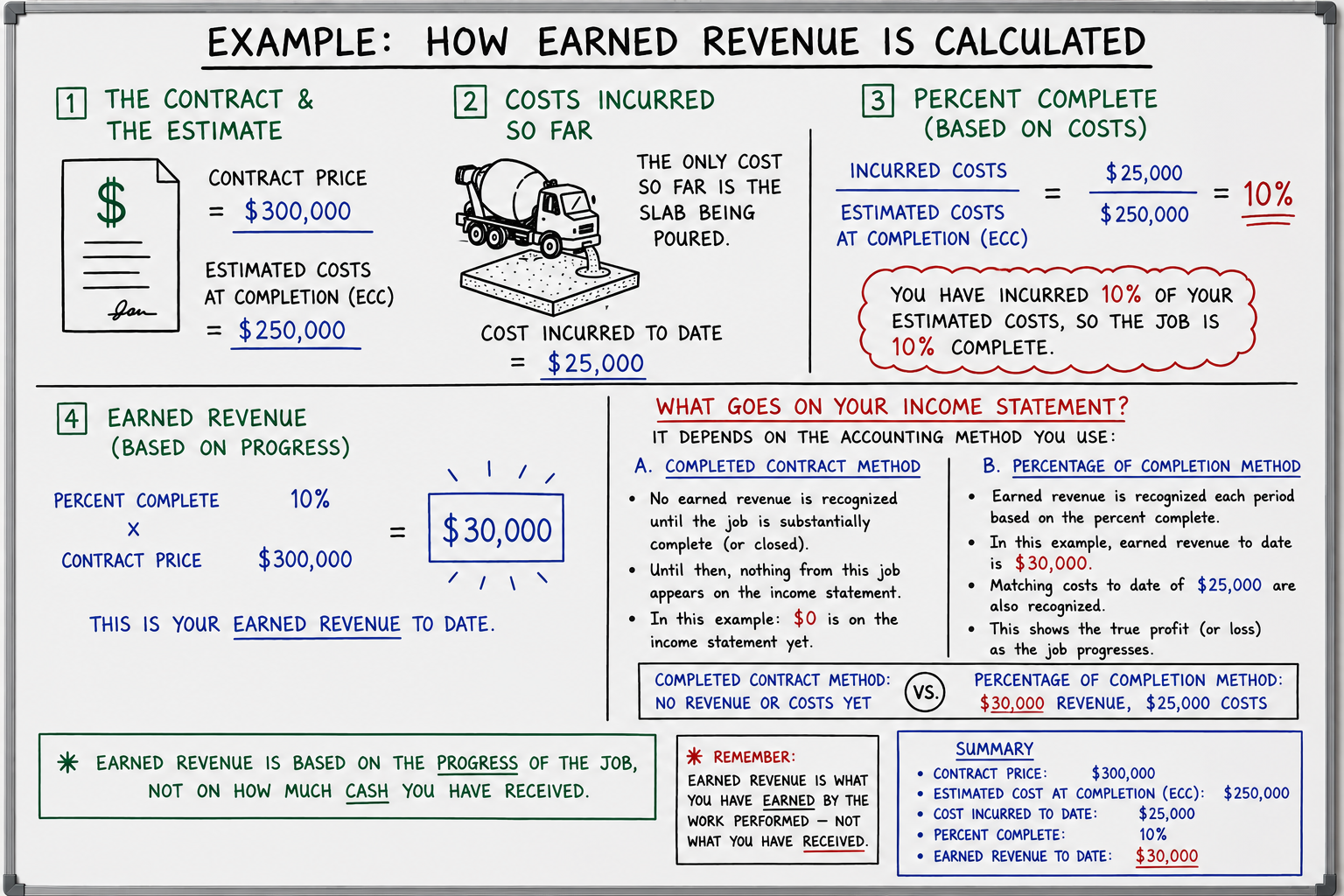

Why? Because if a home builder receives a $100,000 down payment, for example, before hardly any work is done, and posts that money straight to Sales, AND has incurred $10,000 in job costs so far, and posts that straight to Cost Of Sales, the Income Statement for that month would show $90,000 in Gross Profit that HAS NOT BEEN EARNED YET. In other words, the profit would be way over stated.

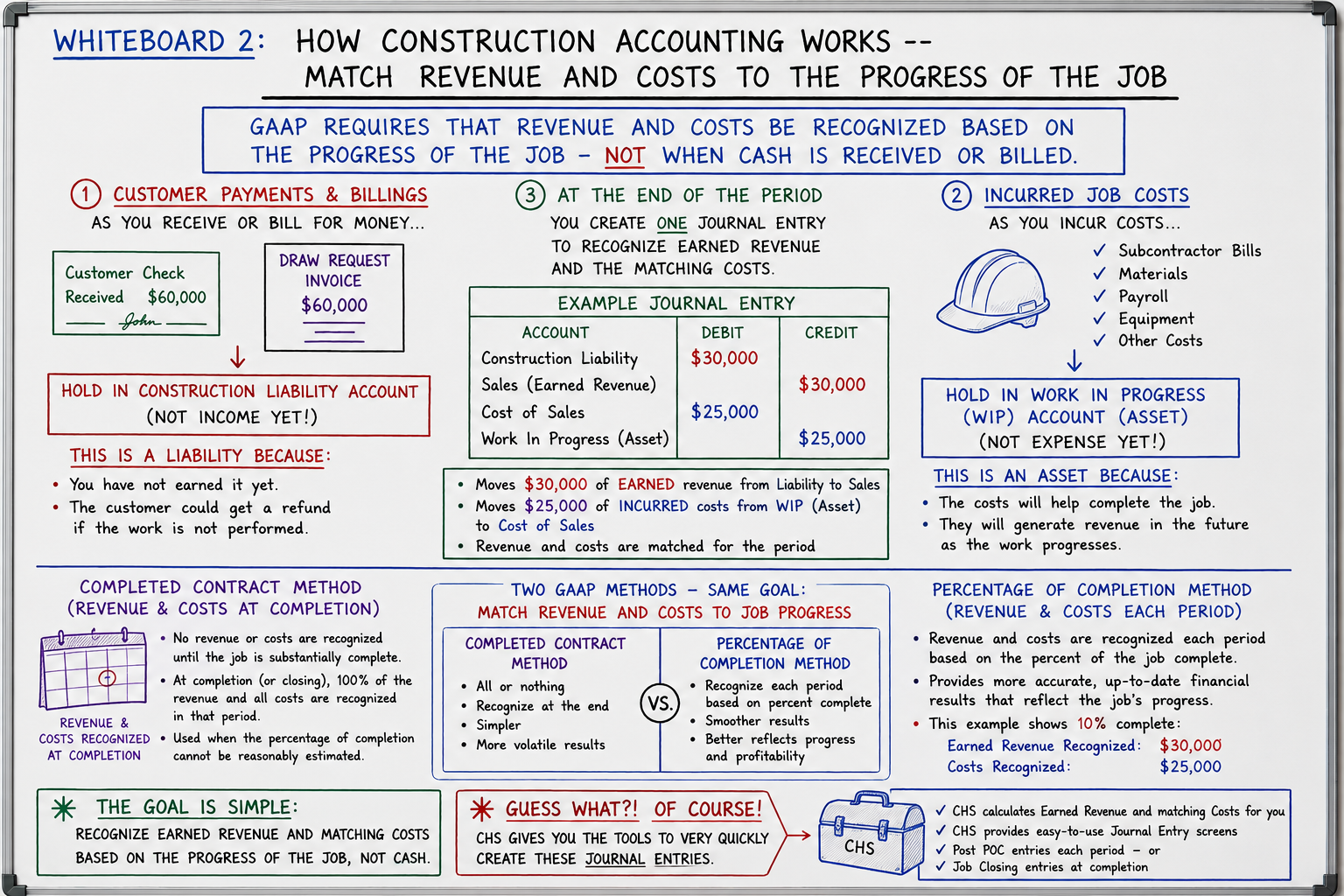

So, at the end of selected periods, usually each month, Earned Revenue must be calculated for every job, which can take hours and hours UNLESS you have a job costing software like CHS to calculate it for you, AND to provide tools for posting the necessary journal entry, based on your chosen accounting method.

Setting Up Your Books For Periodically Posting Earned Revenue

Include at least one Construction Liability GL Account and a Work In Progress Asset GL Account On Your Chart of Accounts. Post monies received or billed to customer to Construction Liability and Post Incurred Job Costs To Work In Progress, in order to hold both revenues and costs in those accounts until a journal entry moves amounts from those accounts to Sales & Cost Of Sales, respectfully.

See whiteboard below: As you receive or bill for actual money, GAAP suggests that you hold the amounts received or billed in a Construction Liability account UNTIL you move an Earned Income amount for a period from that liability account to a Sales account via a journal entry. GAAP also suggests that all incurred job costs should be held in a ‘Work In Progress’ account until you move the matching costs for the period to a Cost Of Sales account in the very same journal entry. And Guess WHAT?! Of course! CHS gives you the tools to very quickly create those journal entries:

CHS has the tools for gathering the numbers needed, AND then posting a journal entry for either the Percentage Of Completion accounting method, or the Complete Contract accounting method!